Sustainability reporting: understanding the VSME standard for micro and small businesses

On December 17, 2024, EFRAG published the VSME standard, which provides a voluntary reporting framework for small and medium-sized enterprises not subject to the CSRD. What does the VSME entail and what information is required? Why and how to comply? We answer all your questions in this article.

1. In what context does the VSME standard apply and what is its objective?

The VSME standard (Voluntary Sustainability Reporting Standard for non-listed SMEs) is a voluntary sustainability reporting framework specifically designed for micro, small, and medium-sized enterprises that are not listed and do not fall under the scope of CSRD. The final standards were issued by EFRAG on December 17, 2024, following a public consultation from January 22, 2024, to May 21, 2024.

🔎 Focus : The document published on December 17 is a technical opinion and does not yet constitute the official version of the VSME standard. The technical opinion has been sent to the European Commission, which may still decide to make changes before its official release anticipated in 2025.

The objective of the VSME standard is to enable small and medium-sized enterprises to also have a structured and harmonized framework to engage in sustainability. It is thus presented as a "simplified" sustainability reporting standard adapted to the limited means and resources of these enterprises.

Although it is a voluntary reporting framework, SMEs have every interest in complying with the VSME standard in order to:

- Structure and clarify their CSR strategy through a clear identification of their sustainability issues

- Anticipate regulatory changes that are moving toward the generalization of reporting obligations across all companies

- Meet the expectations of their business partners, particularly large companies, in terms of sustainability

- Gain easier access to responsible funding

- Improve their brand image and strengthen stakeholder trust

- Reduce their costs by reducing their environmental impact (energy management, waste management, etc.)

- Fully commit to the low-carbon transition and thus contribute to the European climate goals

2. How is the VSME standard structured?

The VSME standard is a framework structured around two modules:

- A basic module (basic module) that sets the minimum VSME sustainability report requirements. This module includes 11 disclosure requirements structured by type of ESG issue (environmental, social, and governance)

- A comprehensive module (comprehensive module) that sets the additional data that may be required by commercial partners (banks, investors, companies) in addition to the data from the basic module. This module includes 9 disclosure requirements

💡Note: Depending on their specific issues, companies have two options for preparing their VSME sustainability report:

- Use only the basic module (micro-enterprises or SMEs whose sustainability issues are not significant);

- Use both the basic module and the comprehensive module.

The basic module is therefore a necessary prerequisite for using the comprehensive module.

According to EFRAG, the data required for these two modules should allow “to meet a substantial portion of the requests from commercial partners that SMEs currently receive”. However, companies may deem it relevant to sometimes integrate additional data depending on their specific issues to ensure a representative and reliable report.

Each module is accompanied by guidance that provides details on the methodology to follow for each disclosure requirement. Finally, the VSME standard also provides:

- In appendix A, a list of definitions to clarify the various terms used

- In appendix B, a list of typical ESG issues that micro-enterprises/SMEs may identify in their VSME report

- In appendix C, various information intended for users of the VSME sustainability reports, including a contextualization of the different required data with other EU regulations (notably the SFDR regulation)

🔎 Focus: To promote the dissemination and acceptability of this standard among both users and micro-enterprises/SMEs, EFRAG also plans from 2025 onwards to develop a true “VSME ecosystem” including in particular:

> The establishment of an “SME forum” to facilitate stakeholder exchanges;

> The creation of a mapping of relevant sustainability initiatives by micro-enterprises/SMEs (platforms, digital tools, training, etc.);

> The publication of a VSME support guide.

3. What are the main principles of the VSME standard?

Modularity and simplified language

As with the CSRD, the VSME standard sets out the data that allows the company to disclose information on:

- How sustainability issues have affected or are likely to affect its financial situation and performance in the short, medium, and long term

- How the company has had or is likely to have positive or negative impacts on people or the environment in the short, medium, and long term

In practice, however, it proves to be much more "light" in terms of methodology and publication requirements than the ESRS standards. The aim is to strike a balance between, on the one hand, the information expected by business partners and, on the other, the capacity and resources of SMEs.

Its division into two modules and the adoption of a simplified language are two key aspects that allow it to apply to companies of very different sizes, from micro-enterprises (less than 10 employees) to small and medium-sized enterprises (SMEs) with up to 250 employees.

Modularity indeed provides some flexibility in the published information. Furthermore, each module can be supplemented with additional qualitative and/or quantitative information if necessary. The determination of this additional information is at the discretion of each company based on its specific challenges and the expectations of its business partners.

⚠️ Warning: Each chosen module must be completed in full to ensure the compliance of the VSME sustainability report.

“If applicable” principle

One of the essential characteristics of the VSME standard is that, unlike the ESRS standards, it does not require a double materiality analysis. This is indeed replaced by the “if applicable” principle (“where appropriate”), an approach considered more suitable and less costly for small and medium-sized enterprises (SMEs).

In practical terms, the required data should only be disclosed if it applies to the company based on its own characteristics. In other words, when a company chooses not to publish certain data required by the standard, users of the report should then consider that this data does not apply to it.

Publication of the VSME sustainability report

The primary function of the VSME standard is to inform business partners and stakeholders about the consideration of ESG issues within the framework of a bilateral exchange. Therefore, the publication of the VSME report is not mandatory. However, companies are strongly encouraged to do so to enhance their credibility and demonstrate transparency in terms of CSR commitment.

EFRAG has specified a number of points regarding the modalities of this publication:

- If the report is intended to meet the needs of large companies or financial players requiring an annual update, the VSME sustainability report must then be published each year and within a timeframe consistent with the preparation of the financial statements to ensure coherence with the financial report

- Companies may decide to omit the disclosure of sensitive information or classified documents but must then specify this explicitly

- The preparation of a consolidated report is recommended for SMEs that are parent companies of a group. Subsidiaries are then exempt from declaration

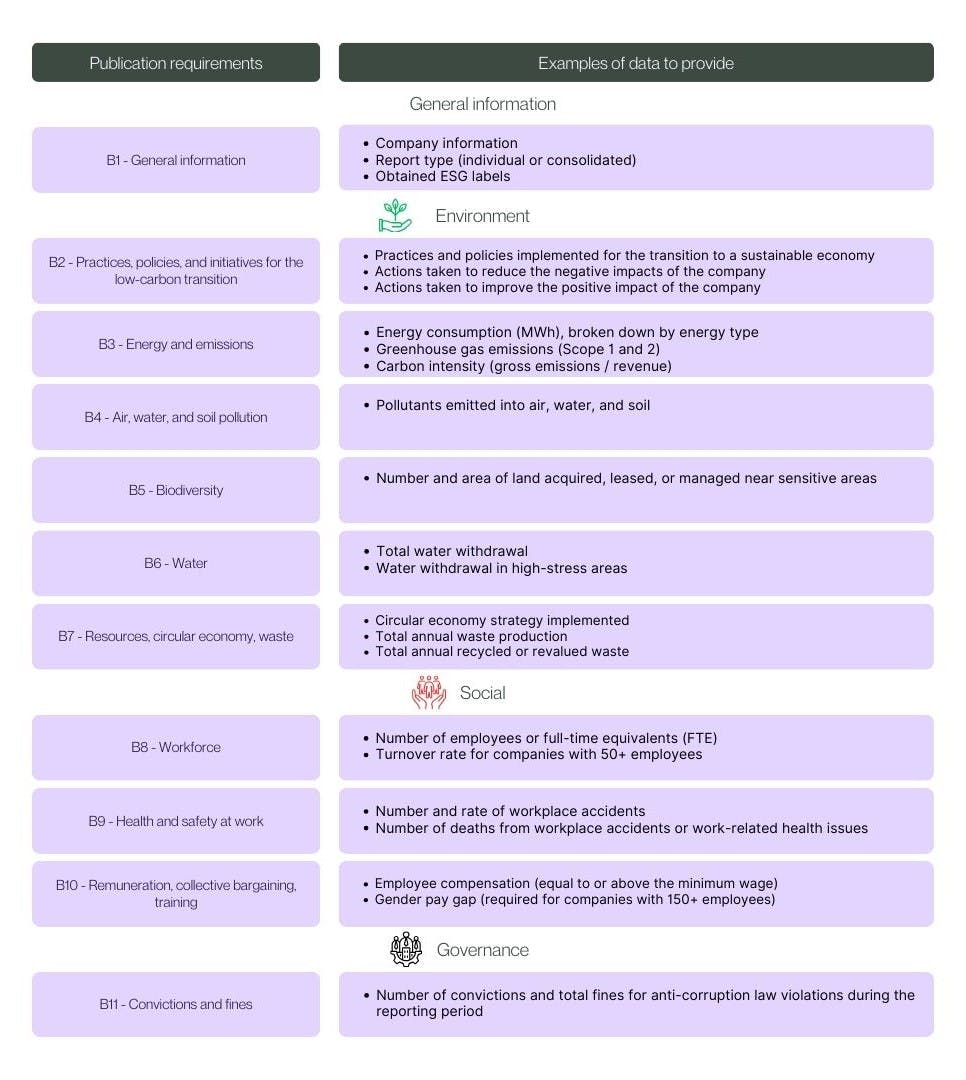

4. What information is required by the VSME standard?

Basic Module

Below you will find the main information required under the 11 disclosure requirements of the basic module.

Regarding the disclosure of greenhouse gas emissions (B3), the standard further specifies that depending on the company, it may be appropriate to also disclose Scope 3 emissions to ensure representative data of the company's emission profile. However, the company is then only required to disclose significant Scope 3 emissions.

💡Note: If the company decides to report its Scope 3 emissions, it must then refer to the 15 emission categories identified by the GHG Protocol.

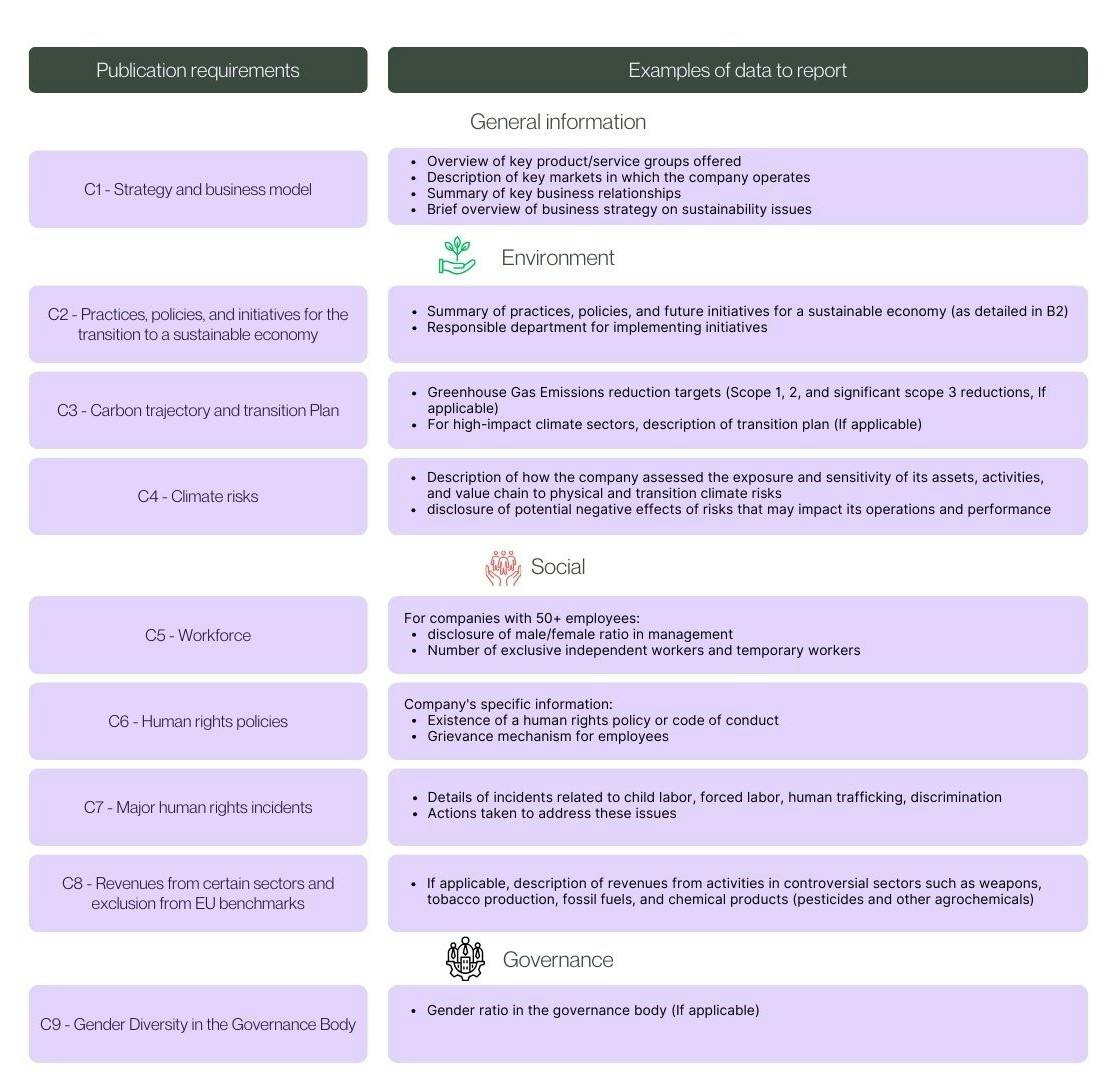

Complete Module

As specified, the complete module is intended for SMEs whose business partners require more in-depth ESG information than what is published under the basic module.

EFRAG specifies that the list of these requirements was determined based on existing laws and regulations and includes the main information necessary to enable an assessment of the company's risk profile (notably as a supplier or borrower).

Below you will find the main information required under the 9 disclosure requirements of the complete module.

5. What best practices to comply with the VSME standard?

The VSME standard therefore represents a real opportunity for small and medium-sized enterprises to engage in sustainability and structure their CSR strategy. However, to ensure the success of the approach and ensure all necessary data is available, it is recommended to proceed in stages:

- Assess the maturity of your company in CSR matters

- Identify the expectations of your business partners and stakeholders to choose the most suitable module

- Proceed to measure the environmental, social, and economic impact of your company notably by conducting a Carbon Footprint assessment

- Establish sustainability goals that are both measurable and realistic (carbon trajectory, waste reduction targets, etc.)

- Gather the necessary data for preparing the VSME report

- Draft the VSME report

- Communicate the report and highlight the results to enhance the company's credibility and retain its stakeholders

👉Contact us for tailored support in implementing your ESG approach. With our SaaS platform, easily collect and centralize your ESG data and receive support from our team of experts

Our latest articles

Responsible Digital: the next step after your Carbon Footprint assessment

Understand the importance of implementing a responsible digital approach after completing your carbon footprint assessment

CSR News - April 2025

Discover the key developments: ongoing projects, standards updates, new official documents.

ESG Data: How to identify, collect, and use them

Learn how to structure your ESG data to better drive your commitments and enhance your sustainable performance

Guide on ESG performance: definition, measurement, and impact on business

ESG performance, a driving force for responsible growth: follow our guide to understand everything in just a few minutes